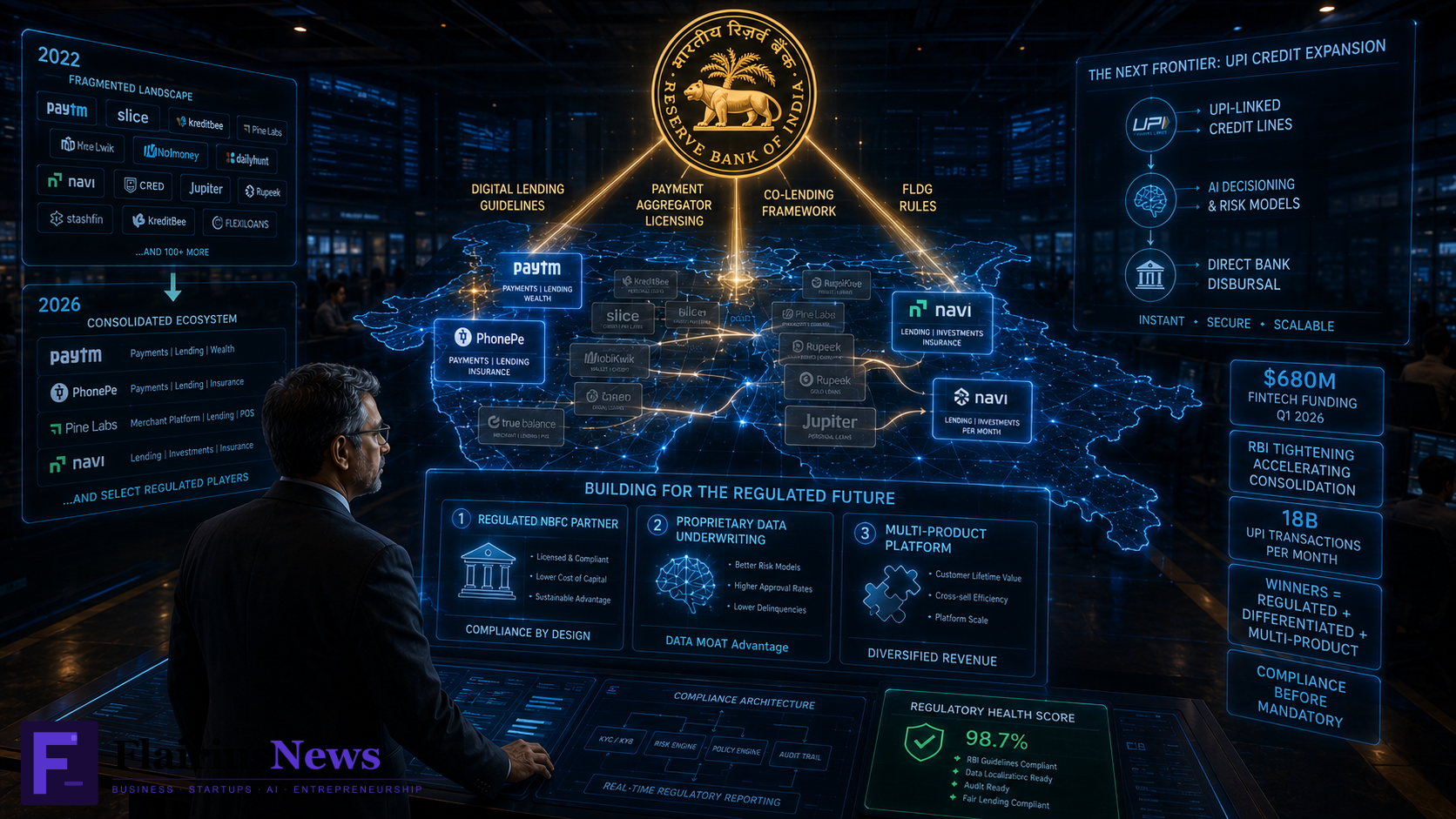

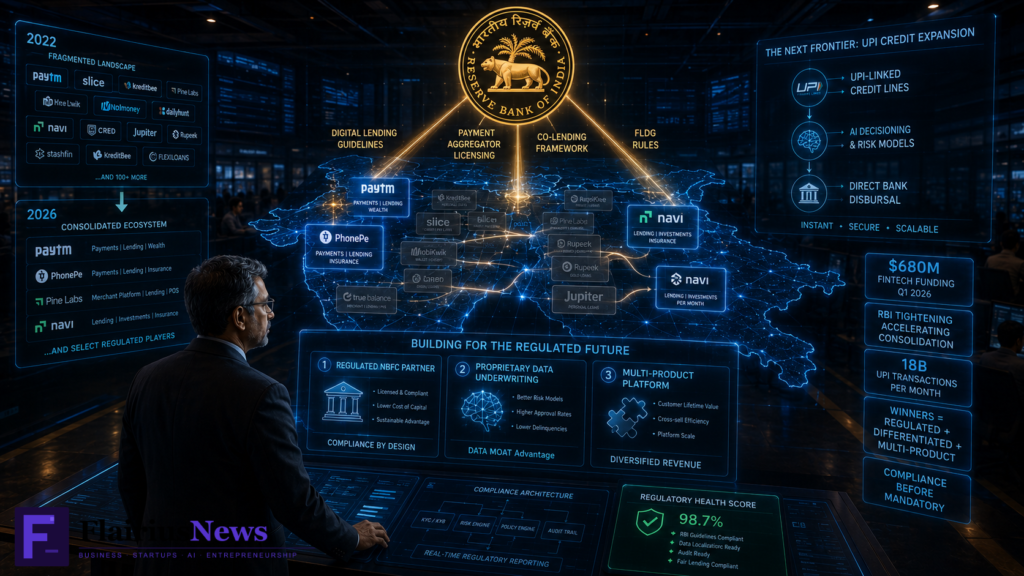

India’s fintech boom produced hundreds of companies. Moreover, it produced many of them in adjacent categories with similar products and overlapping customer bases. Consequently, the consolidation that was always inevitable is now accelerating driven by RBI’s tightening regulatory environment.

In FY26, fintech consolidation is accelerating as RBI rules reshape business models across digital lending, payments, and investment platforms. Furthermore, the companies that are surviving this consolidation phase are not necessarily the ones with the most users. They are the ones with the clearest regulatory compliance posture, the strongest unit economics, and the most differentiated positioning.

What RBI’s New Rules Actually Changed

The Reserve Bank of India has implemented several significant regulatory changes affecting fintech companies in 2024–2026. Specifically, these span digital lending guidelines, payment aggregator licensing, co-lending framework tightening, and new rules on first loss default guarantees.

The digital lending guidelines were the most disruptive. Specifically, they banned the “instant credit” model where fintech companies disbursed loans without the NBFC or bank partner having direct visibility into the borrower relationship. Furthermore, they mandated direct bank account disbursals eliminating the prepaid wallet intermediary layer that many fintech business models depended on.

Consequently, several fintech companies built on that wallet-intermediary model faced existential structural challenges. Some pivoted successfully. Others merged with larger players that had the NBFC or bank partnerships to absorb their user base. Moreover, a significant number simply wound down.

The Winners in India’s Fintech Consolidation

Three types of companies are winning this consolidation phase. Therefore, understanding each profile matters for founders and investors.

First, regulated entities with direct banking relationships. Specifically, fintechs that secured their own NBFC licences or established direct co-lending agreements with scheduled banks before the regulatory tightening have a structural advantage. Furthermore, they can acquire the user bases of companies that could not make the regulatory transition. Consequently, they are growing through the consolidation rather than shrinking.

Second, companies with genuinely differentiated data assets. Specifically, fintech companies that built proprietary underwriting models on unique data UPI transaction history, GST filing patterns, account aggregator data have a risk decisioning advantage that commodity lending platforms cannot match. Moreover, RBI’s regulatory framework actually rewards this differentiation by allowing better-underwriting platforms to expand credit access more safely.

Third, platform businesses with multiple product lines. Specifically, fintechs that built cross-sell revenue combining lending with insurance, investments, or wealth management are more resilient to regulatory changes in any single product category. Furthermore, their customer relationships are deeper, making retention higher during periods of regulatory disruption.

The Impact on India’s Broader Startup Ecosystem

The fintech consolidation has second-order effects across India’s startup ecosystem. Specifically, the engineering and product talent that exits consolidated fintechs is seeding new startups in adjacent categories BFSI AI, compliance technology, and financial infrastructure tooling.

Furthermore, the consolidation creates a cleaner competitive landscape for the survivors. Consequently, the companies that emerge from this phase with regulatory clarity, strong unit economics, and differentiated positioning will face less fragmented competition than they did in 2022.

Moreover, the regulatory tightening is producing better products. Specifically, digital lending products that comply with direct bank disbursal requirements are fundamentally more transparent and consumer-protective than the wallet-intermediary models they replace. Therefore, the regulatory pressure is driving product quality improvement not just survival pressure.

What Comes Next

India’s fintech sector will not stop consolidating in 2026. Furthermore, the RBI has signalled additional regulatory attention on buy-now-pay-later products, cross-border payments, and AI-driven credit decisioning. Consequently, companies building in these areas should assume regulatory clarity will arrive and build compliance infrastructure before it becomes mandatory.

Additionally, the UPI credit expansion enabling credit lines linked directly to the UPI flow represents the next major product frontier in Indian fintech. Moreover, it is one where regulatory compliance and AI decisioning capability are both prerequisites. Therefore, the companies best positioned for the next phase of Indian fintech are those that have used the consolidation period to build both.

Tags: India Fintech Consolidation 2026, RBI Regulation Fintech, Digital Lending India, Indian NBFC, Fintech Winners Losers, UPI Credit India, India Financial Services Startup 2026 Author CTA: Follow Flairius News — sharp takes on AI, business, and India’s startup economy — flairiusnews.com