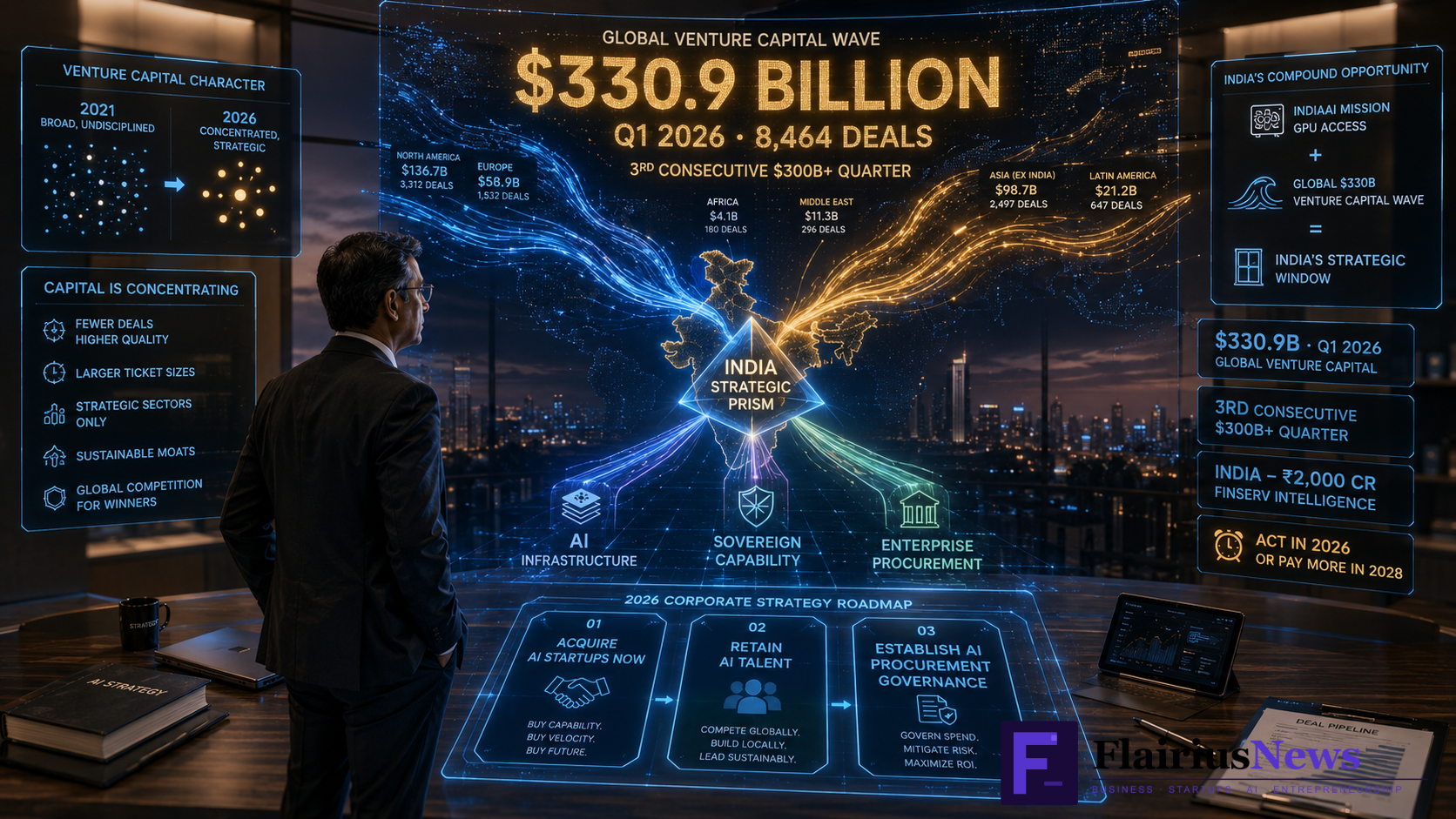

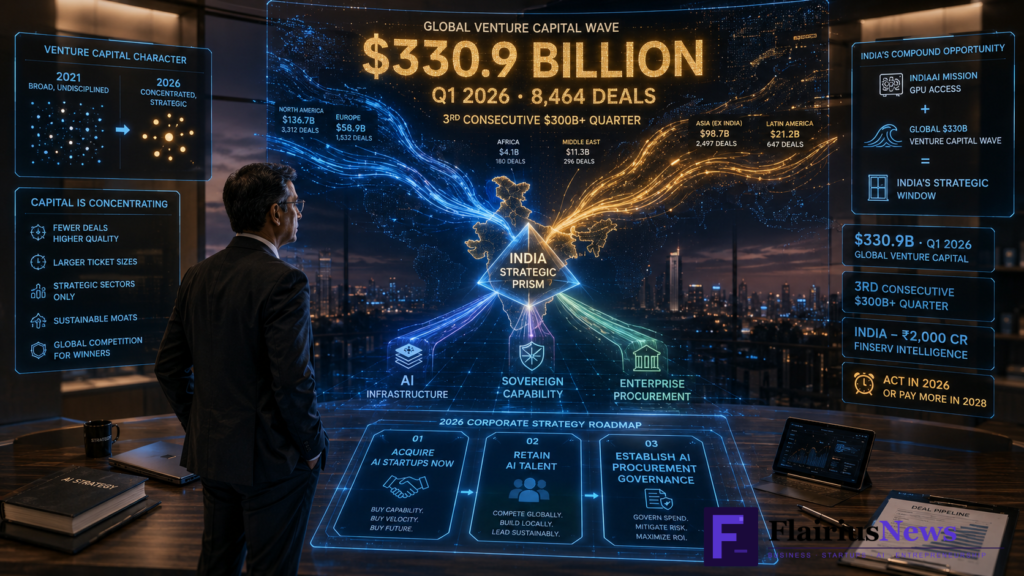

Global venture investment reached $330.9 billion in Q1 2026. Furthermore, this was the third consecutive quarter with over $300 billion in venture deals. Moreover, the 8,464 deals done globally in that single quarter represent the highest deal velocity since the 2021 peak but with a fundamentally different character.

Understanding this character matters for every Indian business leader not just founders and investors.

The Character of the Current Capital Wave

The 2021 venture boom was broad. Capital flowed into consumer apps, growth-stage companies, and almost any credible tech pitch. Consequently, many businesses that should not have raised institutional capital did. Furthermore, valuations disconnected from fundamentals. The bust that followed was predictable.

The 2026 capital wave is concentrated. Specifically, it rewards companies with three characteristics: proximity to AI infrastructure spending, enterprise procurement-readiness, and sovereign capability credentials. Therefore, the businesses attracting the most capital in 2026 are fundamentally different from the ones that led the 2021 surge.

Moreover, defence tech and spacetech have entered mainstream venture discussion. Additionally, semiconductor-adjacent ventures are attracting strategic capital from sovereign wealth funds and national governments not just private venture firms. Consequently, the definition of what constitutes a “venture-backable business” has expanded significantly.

What This Means for Indian Corporate Strategy

For Indian business leaders at established companies, the global venture wave creates three specific strategic implications.

First, the acquisition environment is changing. Specifically, AI-native startups that would have taken five years to build commercially viable products are now building them in 18 months supported by unprecedented capital access and compute availability. Therefore, established Indian companies that wait for organic capability development may find themselves acquiring capabilities at significantly higher valuations or not at all.

Furthermore, Bajaj Finserv’s ₹2,000 crore Finserv Intelligence commitment is the correct strategic response to this environment build or buy capability early, before the market prices it appropriately. Consequently, corporate venture and M&A arms that move in 2026 will have better options than those that move in 2028.

Second, talent competition is intensifying. The global capital wave funds well-compensated AI talent at startups. Moreover, Indian technology companies from TCS to Infosys to the largest Indian conglomerates are competing for the same engineers. Consequently, compensation structures, equity programs, and work environment standards need to evolve to retain the talent that incumbents need.

Third, the procurement conversation is shifting. Specifically, enterprise buyers in India are increasingly evaluating AI vendors both Indian and global for integration into core business processes. Furthermore, they are doing so faster than their procurement processes were designed for. Therefore, establishing clear AI procurement governance which vendors, which data access, which sovereignty requirements is a board-level discussion, not an IT department one.

The India-Specific Opportunity Within the Global Wave

India captures a specific slice of this global capital wave that is different from any other country’s opportunity. Specifically, India’s combination of English-language capability, deep engineering talent, large domestic market, and growing sovereign AI infrastructure gives Indian companies a positioning that neither pure Western nor pure Chinese AI companies can replicate.

Moreover, the IndiaAI Mission has created subsidised compute access that makes AI development more affordable in India than almost anywhere else outside China. Consequently, the global $330 billion wave is one tailwind. India’s domestic policy environment is another. Together, they create a compound opportunity that forward-looking business leaders must actively plan to capture.

The capital is available. Furthermore, the infrastructure is building. Therefore, the only variable remaining is strategic intent the decision to act now rather than wait for certainty that will never fully arrive.

Tags: Global Venture Capital 2026, $330 Billion VC Q1, India Business Strategy, AI Infrastructure Investment, India Corporate Strategy, Venture Capital India, AI Procurement India, Bajaj Finserv Intelligence Author CTA: Follow Flairius News — sharp takes on AI, business, and India’s startup economy — flairiusnews.com